Today we launch a data tool to help people better understand how inflation affects people like them who share similar demographics.

Our two-month research project with Nottingham Civic Exchange, part of Nottingham Trent University, aimed to understand how inflation impacts different people across the UK. Our research has uncovered how inflation rates can be misleading by examining the impact on different demographics including household income and region.

We are advocating for a shift in monetary policy which will move the focus from the headline inflation rate to a more nuanced understanding of how those living on low-incomes are affected by price increases - what we call the ‘breadline inflation rate’. We argue this is a more progressive means to improve economic security.

What we hope to achieve and why we explored this issue

ONS data released in November last year provided a spark for two students at NTU. We’ve been working with them to examine how household spending impacts interest rates. They argued persuasively that the ‘headline’ inflation rate cannot meaningfully tell us how it impacts different demographics in society, including those living in so-called ‘affordable’ towns and cities like Nottingham.

We have produced a tool that allows anyone from across the UK to identify how their spending will be impacted by inflation. We believe the Bank of England should report on their variations within Agents Reports and discuss the variation between different groups regularly to help people become more aware of how their spending is impacted by inflation. This will have the benefit of improving financial literacy and resilience.

Key findings

The data compiled and analysed by the RSA and Nottingham Trent University reveals that around the bottom 30% of earners spend more than they make – indicating financial precariousness is much more widespread than many feared.

Our analysis also found that this group are spending more on essentials than luxuries, indicating debt is likely being used to buy food and pay rent, rather than TVs or smartphones.

With a decade of disruption looming from the challenges and opportunities of automation, as well as Brexit uncertainty, we urgently need a new focus on economic insecurity from policy-makers to support households that previous RSA research demonstrated 40% of which have less than £1,000 in savings.

Stagnation (or even decline) in the living standards of ordinary working families, explored in our recent RSA report Addressing Economic Insecurity is a recurring political theme. Household budgets and indebtedness matters to a growing number of people across the UK as wages stagnate and costs increase, with or without the implications of Brexit being fully known.

How does the Bank of England calculate inflation rates currently?

The Bank of England uses the Consumer Price Index (CPHI) and Consumer Price Index including housing costs (CPIH) as its headline measure. Whilst the inflation rate for different groups across the UK is currently broadly the same this has not always been the case with large variations between different groups and the average.

Living standards of ordinary working families is a recurring political theme and how you spend your household budget matters to a growing number of people across the UK as wages stagnate and costs increase, with or without the realities of Brexit being fully known.

How could we reflect people’s real experience of the inflation rate?

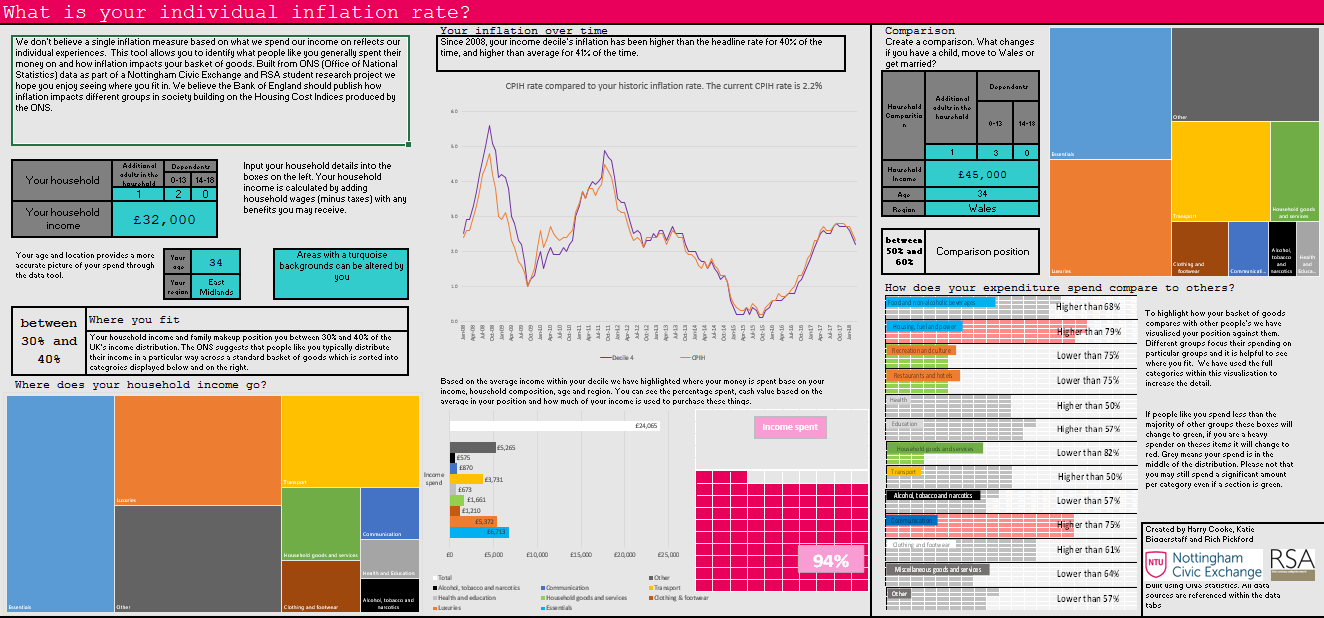

Our data tool demonstrates that inflation is not experienced uniformly by everyone but that rising living costs vary depending on what household’s purchase, with housing costs in particular varying hugely by age and region. To illustrate this, we pulled together stereotypical household profiles using our tool to demonstrate how the inflation rate affects individual households differently, using inflation data covering 2008 to 2017.

-

A stereotypical “Just About Managing” couple, courted by both major parties, aged 35 on an income of £35,000 and living in the East Midlands with two children, have a higher than headline rate of inflation for 51% of the year; higher than average for 60% of the time. The statistics suggest such a couple would spend 102% of their income, indicating a problem with debt for such “Just About Managing” couples.

-

A 65-year old couple in Scotland on an income of £50,000 experience an inflation rate above headline rate for 21% of the year and higher than rate average for 31% of the year.

-

An 80-year old in the North East on £12,000 a year, in the bottom decile of household income, will experience an inflation higher than the headline rate for 64% of the year and higher than the average rate of inflation for 72% of the year. This illustrates how pension poverty remains a problem for many left-behind groups.

-

Meanwhile in London, a 28-year old single adult with a dependent child, on an income of £22,000 pays proportionately more than 93% of the population on housing and fuel costs

- Even a relatively affluent couple of 28-year olds in London on £65,000 – in the top 20% of earners – pay proportionately more than 79% on housing, showing house price inflation extends well into household finances, even though this is not officially reflected in the ONS figures.

Are you average? The Bank of England thinks so

Common sense tells us that different people buy different goods and services. Yet the inflation rate is set from a snapshot of an ‘average’ person and their buying habits.

Whilst having a single figure makes modelling simpler it means that some households are consistently worse off. The headline inflation measure, informed by the CPI and CPIH index, is made from the average person's “basket of goods” that they spend money on. Having an inflation figure set by the ‘average’ person is necessary, but our analysis found there are winners and losers when examining how people actually spend their income.

We recommend that the Bank of England and Government account for the way inflation affects the types of households we’ve profiled by publishing rates related to regional and income profiles, like the ones we have highlighted.

Creating this more nuanced measure should help to inform policy and everyday experiences of people who are economically insecure or worried about how changes to the UK will impact on their household budget.

Download our interactive tool to find out and compare your inflation rate

Read the tool explainer

Find out more about the project here

Related articles

-

Our social insecurity system

Hannah Webster

How can we regenerate our social security system to remove insecurity and ensure everyone is receiving the support they need to survive?

-

Using economic strategies to improve health outcomes

Ian Burbidge

Ian Burbidge on the importance of an inclusive economy that provides equitable healthcare to the public.

-

A healthy economy?

Ian Burbidge Will Grimond

Covid shows us how our health and the economy are linked. Politics has been slow to catch up on the connection.

Join the discussion

Comments

Please login to post a comment or reply

Don't have an account? Click here to register.

The article gives the implication that many people today have to ‘live beyond their means’. Belonging myself to a generation whose upbringing was to always ‘live within your means’ - I need to understand whether the people you refer to ‘have to’ or ‘choose to’ live beyond their means’. Are your statistics possibly warped because of an increasing number of people realising that today’s culture allows them to live massively beyond their means while others are ‘more old-fashionly’ living within theirs. I do feel that so many of today’s problems are because expectations are so outstripping reality and yet - it is still possible to meet some people very happily living modestly and well within their modest means.

I can see the merit of an approach that is more refined than the single average basket but it needs to be simple enough for people to follow and easy enough for the Treasury to use. In applying this to our own situation I found the assumptions about discretionary expenditures to be grossly inaccurate (so not better than the universal average basket of goods). Should such a tool not concentrate on some explicit level of essentials, not least because some pricing effects, such as taxes on legal drugs, are designed to influence consumption, so should not be counted as inflation. If this were applied then many of these households would not need to spend more than they earn (but might choose to).